Does Your Portfolio Company Have Enough Sales People?

Part 1 of this series established a go-to-market framework for private equity managers. Part 2 examined the leadership element of this framework: selecting the right leadership to drive top-line growth to the next level. Part 3 addressed the strategy behind the framework. Part 4 below addresses structural components of the revenue growth model.

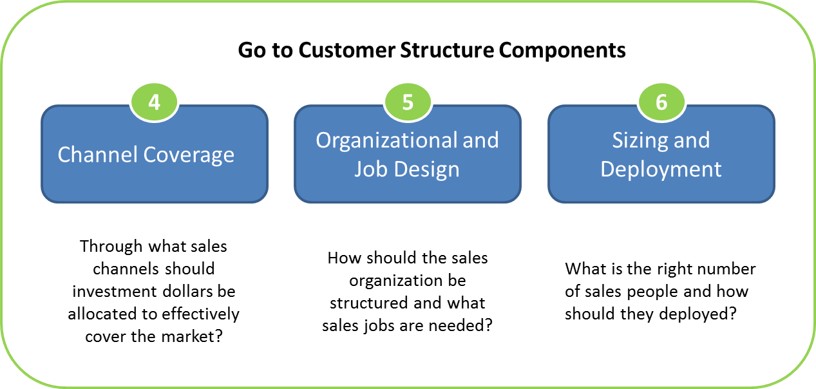

It has been six months since the acquisition. The PE firm has replaced sales leadership and adjusted the portfolio company’s sales strategy to reinvigorate top-line growth. But does the company now have the right number of sales people in the right roles to meet growth objectives? Because headcount is typically the largest component of sales costs, getting this question right is crucial to the financial health of the organization. Channel coverage, organization and job design, and sales force sizing and deployment represent three structural components of the revenue growth model.

1. Channel Coverage: The goal for coverage is to find the most cost-effective means to cover the greatest portion of the market. Early-stage and fast-growth companies often experience a period of growth through simple scaling of seller headcount. This may work well for a time. However, when the company’s offerings expand or business objectives change, this approach can lead to “algorithm failure” where the marginal rate of return from additional sales headcount brings diminishing returns. Coverage inefficiencies also occur from over-reliance on a single channel such as direct field sales. Some sales strategies call for a primarily direct field sales model, such as selling complex, enterprise solutions. Other sales strategies call for primarily inside direct. Still others rely heavily on partners. Most companies require a blend of resources, including direct, indirect, field and inside resources along with a myriad of pre-sales, post-sales, support and specialist overlay positions. The operating partner and sales leadership must examine whether there is an opportunity for new or innovative ways to cover the accounts of the portfolio company. A properly designed coverage model can result in revenue growth while also achieving a reduction in overall cost of sales.

2. Organization and Job Design: Does the company have the right sales jobs and roles? Has leadership clearly defined the jobs? Sales jobs regularly become obsolete, overly expensive, corrupted or capacity-constrained. How should PE firms prevent these issues from happening? First, ensure roles reflect the portfolio company’s sales strategy. A sales strategy will fail without well-constructed job roles driving its execution.

Why are sales jobs so important and relevant in the world of PE growth? Take the recently acquired company noted at the beginning of this article, for example. Their legacy sales force has grown complacent and is simply farming existing customers. Time has shifted from high-value account development and selling activities to lower-value back-office and customer service activities. Net-new acquisition has stalled, making it impossible to achieve growth goals the new PE owner established. If jobs are sub-optimal, then growth will be too.

The seller is the primary role responsible for driving growth. Problems affecting sellers cause deeper issues: misalignment of sales representatives and strategy as well as stagnated seller productivity. Poor job design affects growth equity firms the most because the basis of their investment thesis is revenue growth, not just cost cutting. The fact that growth primarily falls on the sales representatives’ shoulders indicates how vital sellers are to both short-term and long-term value realization.

3. Sizing and Deployment: Resource deployment is the mechanism to physically or virtually deploy resources against the market. Deployment is a major challenge; it is difficult for companies to understand the correct balance between current workload and opportunity.

Operating partners and sales leadership should periodically examine territory sizes and account loads to uncover areas of excess capacity as well as capacity constraints. It is also worthwhile to compare the portfolio company to industry peers. Headcount metrics can help better understand ratios (current vs. best in class) such as “lead gen per rep,” manager span of control, inside vs. field reps and post-sales “resource per rep.” For example, how does span of control at the acquired organization compare to the 8:1 average? Are there circumstances that justify a variation?

Resource deployment is a critical lever for meeting sales targets. Basic math suggests a $100M sales goal requires 100 sellers if each seller has capacity to produce $1M worth of sales. However, this math assumes the company already has an optimal coverage model. It does not take into account productivity gains from lower-cost overlay resources, nor does it consider territory sizes. This is where deployment becomes tangible. The portfolio company must rationalize and align resources to hit the growth number.

Growth-focused PE firms understand the need to demonstrate top-line growth in order to maximize EBITA and therefore receive a higher exit multiple. A portfolio company’s sales strategy should obviously receive significant attention, but sales structure components are also essential. The sales structure is critical to ROI because this is where most sales costs reside. Too many sales representatives wastes money; too few sellers leads to lost revenue growth opportunities. Getting the right number of sales representatives and overlay resources is vital to success!

Start the sales structural review of the portfolio company by asking a fundamental question: Do we have the right resources covering the right customers? If not, a company’s growth strategy will likely fail.

Our next blog in this series will focus on Management, including how to measure and manage productivity.

Co-author: Chris Semain is a principal and a private equity practice leader at Alexander Group.

Learn more about the Alexander Group’s private equity practice.

Contact an AGI private equity practice leader.